After the 62 mph straight-line winds tore through Middle Tennessee on April 16, 2026, many homeowners in Mt. Juliet and Hendersonville realized that a few missing shingles were just the tip of the iceberg. Filing a roof insurance claim nashville residents can actually rely on shouldn’t feel like a gamble against storm chaser scams or confusing policy language. You’ve worked hard for your home, and you shouldn’t have to settle for a patchy, mismatched repair that tanks your property value.

We understand the anxiety that comes with rising premiums and the frustration of deciphering the difference between Replacement Cost Value and Actual Cash Value. It’s a complex system, but you don’t have to face it alone. This guide provides the expert roadmap you need to navigate the process with total confidence. We will reveal how to utilize Tennessee’s “reasonably uniform appearance” standards to your advantage, why the one-year filing deadline is non-negotiable, and the specific steps to ensure your insurance carrier honors the full scope of your restoration. From the first inspection to the final shingle, we’re here to help you protect your investment and restore your peace of mind.

Key Takeaways

- Learn how to leverage Tennessee’s “Matching Law” to ensure a uniform appearance and potentially secure a full roof replacement.

- Master the exact step-by-step process for a successful roof insurance claim nashville homeowners need to follow to avoid common filing errors.

- Discover the critical difference between RCV and ACV policies so you can accurately predict your out-of-pocket costs before work begins.

- Identify the red flags of out-of-state “storm chasers” and learn why local expertise is your best defense against insurance fraud.

- Understand the vital importance of having a trusted local contractor present during the adjuster’s inspection to advocate for your home’s protection.

Understanding Tennessee Roof Insurance: Key Terms and State Laws

Starting a roof insurance claim nashville homeowners can trust begins with understanding the fine print of your policy. Many people assume their insurance covers every disaster, but the specific terms on your Declarations Page dictate your financial responsibility. In Middle Tennessee, most residents carry an “Open Perils” policy. This means your insurer covers all damage unless the policy specifically excludes it. Others may have a “Named Perils” policy, which only provides coverage for specific events like fire or hail. Knowing which one applies to your homeowner’s insurance policy is the first step toward a successful restoration.

Your deductible is another critical factor. This is a fixed out-of-pocket cost you agreed to when you purchased your policy. In Tennessee, it’s legally required that homeowners pay this amount. Be wary of any contractor who offers to “waive” or “cover” your deductible. This practice is considered insurance fraud in our state. We always advocate for transparency because protecting your home shouldn’t involve legal risks. We want you to feel confident that your claim is being handled with the highest ethical standards.

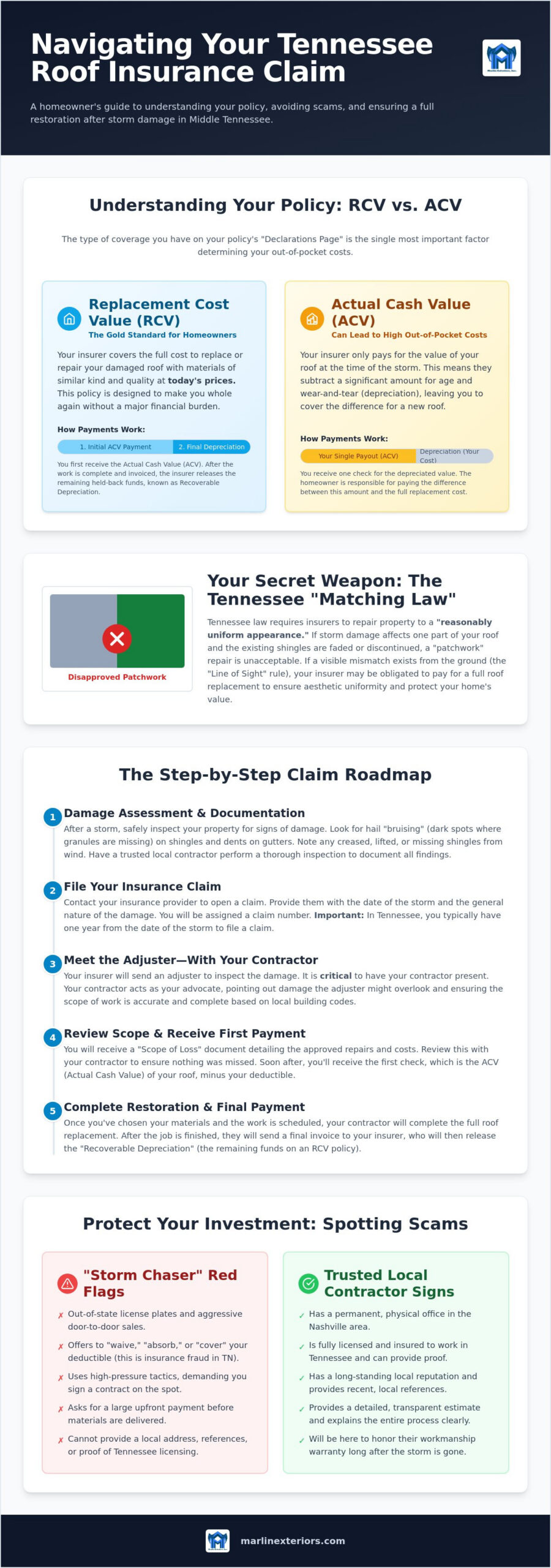

The Tennessee Matching Law: Your Secret Weapon

Tennessee law requires that insurance companies maintain a “reasonably uniform appearance” during repairs. If a storm damages only one slope of your roof and the existing shingles are discontinued or faded, the insurer may be required to replace the entire roof. This prevents a “patchwork” look that would otherwise lower the resale value of your Mt. Juliet home. Under this standard, if a visible mismatch exists from the ground level, the “Line of Sight” rule often triggers a full replacement. Tennessee law essentially mandates that insurers must replace the whole roof if a partial repair cannot achieve aesthetic uniformity.

RCV vs. ACV: Why Your Policy Type Changes Everything

Replacement Cost Value (RCV) is the standard we recommend for Nashville neighborhoods. It covers the actual cost to replace your roof at today’s prices. In contrast, Actual Cash Value (ACV) policies only pay the depreciated value based on the age of your roof. If you have an older roof with an ACV policy, your out-of-pocket costs could be significantly higher. You can find this designation on your Declarations Page under the “Loss Settlement” section. RCV is the gold standard because it ensures your home value is fully restored without a heavy financial burden on your family.

When you have an RCV policy, the insurance company often sends two payments. The first check is the ACV, which is the depreciated value of the roof. The remaining amount, known as Recoverable Depreciation, is held back until the work is complete. Once we provide the final invoice showing the project is finished, the insurance company releases those funds to cover the full cost of your roof insurance claim nashville project. This system ensures the money is used specifically for the intended home improvements.

Identifying Storm Damage: Hail, Wind, and the Middle TN Climate

Middle Tennessee has long been known for its scenic landscapes, but for homeowners, it also brings unique environmental challenges. We are situated in a region that weather experts often refer to as an extension of “Tornado Alley.” This geographic reality means your roof is regularly subjected to high-velocity winds and volatile pressure changes that can compromise even the sturdiest asphalt shingle systems. When you’re considering a roof insurance claim nashville weather events often serve as the primary catalyst for necessary restoration.

Hail damage is particularly deceptive because it rarely looks like a puncture. Instead, look for “bruising,” which appears as dark, circular indentations where the shingle’s protective granules have been knocked away. This granule loss exposes the underlying fiberglass mat to harsh UV rays, causing it to become brittle and fail long before its time. Wind damage presents differently. Rather than impact marks, you might see shingles that are lifted, curled, or have a distinct horizontal crease where the wind caught the edge and snapped the sealant strip. These compromised seals allow water to drive underneath the shingles during the next heavy rain.

Ignoring these subtle signs leads to secondary damage that can quickly spiral out of control. A small, undetected leak today transforms into saturated insulation, ceiling stains, and even structural rot within the attic space. Catching these issues early is the only way to ensure your home remains a safe, durable sanctuary for your family. If you’ve lived through a recent storm, it’s a good idea to contact a local specialist for a professional look before a minor problem becomes a major expense.

The Nashville Storm Calendar: When to Be Alert

Tennessee typically experiences its most severe weather during the Spring and Fall months. April and May often bring the highest frequency of tornadic activity, while October and November can see sharp cold fronts that produce damaging straight-line winds. We recommend requesting a professional evaluation after any storm event where wind gusts exceed 50mph. For more details on localized weather patterns and how they affect your property, you can read our storm damage roof repair tn guide.

Why Ground-Level Inspections Aren’t Enough

Standing in your driveway with a pair of binoculars won’t reveal the full story. Many forms of hail damage are completely invisible from the ground, especially on the upper ridges or steep pitches of your home. We utilize high-resolution photography and detailed physical inspections to document the precise extent of the damage. This evidence is vital for a successful roof insurance claim nashville. Safety is our top priority; please don’t attempt to climb a ladder yourself on a steep or potentially weakened roof. Professional documentation provides the clarity and proof your insurance adjuster will need to see.

The Step-by-Step Tennessee Roof Insurance Claim Process

Successfully managing a roof insurance claim nashville homeowners often find, requires a structured approach rather than a reactive one. You shouldn’t simply wait for the insurance company to tell you what they’ll pay. Instead, you need a proactive plan that ensures every piece of storm damage is documented and accounted for before the first shingle is even pulled. We’ve spent 20 years walking these neighborhoods, and we’ve refined a five-step process that protects your home and your wallet.

- Step 1: Professional Inspection. Before you call your agent, let a specialist document the damage. We provide high-resolution photos and a detailed report of hail bruises or wind-creased shingles so you have proof ready to go.

- Step 2: Filing the Claim. Contact your insurance provider with your documented evidence and the specific date of loss. This ensures your claim is filed correctly from the very beginning.

- Step 3: The Adjuster Meeting. This is the most critical stage. We meet the adjuster at your home to walk the roof together. Having a professional advocate present ensures that the adjuster doesn’t overlook subtle but significant damage.

- Step 4: Reviewing the Scope of Work. Once the insurance estimate arrives, we review it line-by-line. We make sure the pricing reflects local Nashville material costs and includes all necessary components like flashing and ridge vents.

- Step 5: Production and Final Inspection. After the scope is agreed upon, we begin the restoration using high-quality asphalt shingle systems. We conclude with a thorough final inspection to ensure your home is fully protected.

Winning the Adjuster Meeting

Bridging the gap between what an adjuster sees and what a roofer knows is vital for a successful roof insurance claim nashville. Adjusters often work under strict corporate guidelines that might prioritize minor repairs over full replacements. Marlin Exteriors, Inc. acts as your professional advocate by providing a ‘Scope of Loss’ comparison. When we’re on the roof with the adjuster, we point out the specific physical evidence that justifies a full restoration under Tennessee standards. This collaborative but firm approach ensures you receive the coverage you’re entitled to under your policy.

Reviewing Your Insurance Estimate

Deciphering the paperwork from your insurance company can be overwhelming. Most carriers use software like Xactimate or Symbility to generate ‘Line Items’ for every part of the repair. If the insurance estimate is lower than the actual cost of high-quality materials, don’t panic. We handle the supplement process for you. This involves submitting additional documentation for hidden damage, such as deck rot, that is only discovered during the tear-off phase. This ensures the insurance company covers the true cost of restoring your home to its original value.

Avoiding Scams: Local Neighbors vs. Storm Chasers in Nashville

After a major weather event hits Middle Tennessee, your neighborhood will likely see a surge in door-to-door solicitors. While some are legitimate, many are out-of-state “storm chasers” who follow hail maps across the country. These companies want to sign as many contracts as possible before moving to the next disaster zone. For a successful roof insurance claim nashville homeowners must distinguish between these temporary operations and established local professionals who will be here long after the clouds clear.

One of the most dangerous red flags is a contractor offering to “waive” or “absorb” your insurance deductible. In Tennessee, this is not a helpful discount; it is a violation of state law. Any contractor willing to cut corners with the legal requirements of your policy will likely cut corners on your roof installation too. Look for out-of-state license plates or high-pressure tactics that demand an immediate signature. A true local neighbor will give you the space to make an informed decision without aggressive sales pitches.

Always verify a company’s standing through the Tennessee Department of Commerce & Insurance portal. A valid TN Contractor License and up-to-date workers’ compensation insurance are non-negotiable requirements for any project. Marlin Exteriors, Inc. has maintained our roots in Mt. Juliet for over two decades because we believe in accountability and community ties. If you have questions about the validity of a claim or the condition of your shingles, reach out to us for an honest assessment from a team that actually lives where you do.

Questions to Ask Any Roofer Before Signing

Before you commit to a contract, ask for a physical office address in Middle Tennessee. A “virtual office” or a hotel room is a sign that the company may disappear once the checks are cashed. Ask for local references from nearby areas like Brentwood or Gallatin. Seeing a completed project in your own community is the best proof of quality. For a more detailed breakdown of what to look for, check out our roofing contractors mt juliet tn checklist.

Why Local Expertise Matters for Warranty Claims

Labor warranties are only as good as the company that provides them. If a storm chaser company moves to a different state next month, your 10-year labor warranty becomes worthless. A local labor warranty is backed by a neighbor you can actually call if a leak develops three years down the road. The 20-year history of Marlin Exteriors, Inc. in Mt. Juliet provides long-term peace of mind because our clients know exactly where to find us. We treat every roof insurance claim nashville project as an investment in our own community’s safety and property values.

Restoring Your Peace of Mind with Marlin Exteriors, Inc.

Navigating a roof insurance claim nashville homeowners find is about more than just fixing a leak; it’s about restoring the sanctuary you call home. We believe that professional restoration should be defined by honest communication and a total commitment to quality. For over 20 years, Marlin Exteriors, Inc. has focused on building trust with our neighbors in Middle Tennessee by providing clear answers and reliable results. When you partner with us, you aren’t just hiring a contractor; you’re gaining a dedicated guide who understands every nuance of the restoration process.

We take the heavy lifting off your shoulders by managing the complex documentation required by insurance carriers. From providing high-resolution photo evidence to attending the adjuster meeting on your behalf, we ensure your claim is handled with accuracy and integrity. Our team identifies every necessary line item, including the “hidden” damage that others might miss, so your home receives the full coverage it deserves. This proactive approach minimizes your stress and ensures that your property value is fully protected for the long term.

Your home deserves the best materials available. Marlin Exteriors, Inc. specializes in high-quality asphalt shingle systems that are designed to withstand the volatile Tennessee climate. Our crews treat your property with the same respect we would show our own homes. This means we focus on meticulous installation and a thorough final cleanup that leaves your yard exactly as we found it. We want you to feel a sense of relief when you see your new roof, knowing it was built to last by people who care about your community.

More Than Just a Roof: Comprehensive Exterior Care

A storm rarely affects just your shingles. We provide a seamless restoration experience by coordinating repairs for your gutters and siding alongside your roof replacement. This holistic approach ensures that your entire home’s exterior works together as a unified system of protection. Marlin Exteriors, Inc. has spent decades serving families in Mt. Juliet, Lebanon, and the greater Nashville area, and we take pride in being a one-stop resource for property restoration. For a deeper look at local standards, you can read our roofing nashville tn guide.

Ready to Start Your Restoration?

Starting the process is simple and transparent. When you contact us after a storm, we’ll schedule a no-obligation assessment to evaluate the condition of your home. During your first consultation, a specialist from Marlin Exteriors, Inc. will walk you through our findings and explain how we can assist with your roof insurance claim nashville project. We provide clear timelines and honest advice so you can make the best decision for your family. Don’t let storm damage linger and cause structural issues later. Schedule your expert roof inspection with Marlin Exteriors, Inc. today!

Secure Your Home’s Future Today

Restoring your property after a Middle Tennessee storm doesn’t have to be a source of anxiety. By understanding the Tennessee Matching Law and recognizing the subtle signs of hail bruising, you’ve already taken the most important steps toward a successful roof insurance claim nashville. Your choice of contractor is your strongest defense against predatory out-of-state “storm chasers.” You deserve a partner who stays in the community long after the repairs are finished.

At Marlin Exteriors, Inc., we bring over 20 years of Middle Tennessee roofing expertise to every project. We are locally owned and operated right here in Mt. Juliet; we take pride in offering expert guidance through the entire insurance claims process. We’ll stand by your side during the adjuster inspection and ensure your home is restored with the highest quality asphalt shingle systems. Don’t let undetected damage compromise your most valuable asset.

Protect your home-get a professional storm damage inspection from Marlin Exteriors, Inc. today! We look forward to helping you safeguard your investment and giving you the peace of mind you deserve.

Frequently Asked Questions

Will filing a roof insurance claim in Tennessee make my rates go up?

No, Tennessee insurance companies cannot single you out for a rate increase simply because you filed a claim for an “act of nature” like hail or wind. Your insurer is prohibited from raising your individual premium based on a weather-related event. However, rates can potentially increase for an entire geographic area if a major storm causes widespread damage across Middle Tennessee, regardless of whether you personally filed a claim.

How long do I have to file a roof claim after a storm in Tennessee?

Most homeowners in our state have exactly one year from the date of the storm to file a roof insurance claim nashville carriers will accept. While Tennessee has a three-year statute of limitations for property damage, your specific insurance policy usually dictates a much shorter window. It’s vital to review your policy language immediately after a storm to ensure you don’t lose your right to coverage.

Can I choose my own roofing contractor, or does insurance pick one for me?

You have the absolute legal right to choose any contractor you trust to perform repairs on your home. While insurance companies often suggest “preferred vendors,” you aren’t obligated to use them. Selecting a local neighbor who understands Mt. Juliet building codes ensures your home is restored by a professional who is accountable to you and the local community rather than the insurance carrier.

What happens if the insurance company denies my roof claim?

If your claim is denied, you can request a re-inspection or file a formal appeal with your insurance provider. We often recommend having a professional contractor present for the second inspection to point out specific damage the first adjuster might have missed. If the dispute remains unresolved, you can contact the Tennessee Department of Commerce & Insurance to file a complaint and seek regulatory assistance.

Is it illegal for a roofer to pay my insurance deductible in Tennessee?

Yes, it is strictly illegal for a contractor to pay, waive, or “absorb” your insurance deductible in Tennessee. This practice is considered insurance fraud and can result in legal trouble for both the homeowner and the roofer. A trustworthy local specialist will always maintain high ethical standards and help you understand your legal financial responsibility as defined by your insurance policy.

How do I know if my roof has enough damage to warrant a claim?

Determining the extent of damage requires a professional physical inspection on the roof surface. Many forms of storm damage, such as hail bruising or subtle granule loss, are completely invisible from the ground. We look for specific markers that indicate your shingles’ protective layers are compromised. Catching these issues early is essential for a successful roof insurance claim nashville and prevents long-term structural rot.

Does the Tennessee Matching Law apply to partial roof repairs?

Yes, the Tennessee “Matching Law” requires that any repairs result in a “reasonably uniform appearance.” If your existing shingles are faded or discontinued, a partial repair would create a mismatched, patchwork look that devalues your home. In these cases, the law often requires the insurance company to replace the entire roof to maintain aesthetic uniformity and protect your property’s resale value.

What is the difference between a roof repair and a full roof replacement in a claim?

A roof repair focuses on fixing a specific, limited area of damage, while a full replacement involves a complete tear-off and installation of a new shingle system. In the context of an insurance claim, the decision usually depends on the severity of the storm damage and the ability to match existing materials. If a “reasonably uniform” repair isn’t possible, a full replacement is typically required to restore the home’s integrity.